Planning for retirement involves careful budgeting to help manage expenses and maintain financial stability. A well-structured retirement budget considers various income sources, anticipated expenses, and potential changes in spending patterns. By accounting for these factors, you can create a practical plan for managing your finances throughout retirement.

Retirement Budget Guidance: Estimating Income

Understanding expected income sources is the foundation of a retirement budget. Common sources include:

- Social Security Benefits: Estimating monthly benefits[1] based on work history and claiming age can provide insight into a portion of retirement income.

- Pension Payments: For those with employer-sponsored pensions, reviewing payout options and tax implications is important.

- Retirement Account Withdrawals: Withdrawals from 401(k) plans, IRAs, and other retirement accounts should be planned to balance income needs and tax considerations.

- Annuities and Passive Income: Annuities, rental income, dividends, and other investment returns can contribute to financial stability in retirement.

Essential Living Expenses

Fixed costs often make up a significant portion of retirement expenses. These include:

- Housing Costs: Whether maintaining a mortgage, downsizing, or renting, housing expenses remain a key budget item.

- Utilities and Home Maintenance: Electricity, water, internet, and routine home repairs should be accounted for.

- Food and Groceries: Estimating grocery and dining expenses helps maintain a realistic budget.

- Healthcare Costs: Medicare premiums, supplemental insurance, prescriptions, and out-of-pocket medical expenses should be carefully considered.

Discretionary Spending

Retirement often provides more time for leisure activities, travel, and hobbies, all of which should be factored into a budget.

- Entertainment and Hobbies: Costs for recreational activities, club memberships, and hobbies should be planned for.

- Travel Expenses: Whether traveling locally or internationally, budgeting for transportation, lodging, and activities is important.

- Gifts and Charitable Giving: Donations and gifts to family or charitable organizations may be part of planned expenses.

Planning for Inflation and Unexpected Costs

A retirement budget should account for potential cost increases over time.

- Inflation Impact: Rising prices affect daily living costs, making it important to plan for gradual increases.

- Emergency Fund: Setting aside funds for unexpected expenses[2] such as home repairs or medical emergencies can provide financial flexibility.

- Long-Term Care Considerations: Assisted living, in-home care, or nursing home expenses may be necessary later in retirement.

Adjusting the Budget Over Time

A retirement budget is not static and should be reviewed periodically to reflect changes in your income, expenses, and personal circumstances.

- Spending Adjustments: As your retirement progresses, spending patterns may shift, requiring budget modifications.

- Tax Considerations: Understanding how withdrawals from different accounts impact taxable income can help with planning.

- Estate and Legacy Planning: Allocating funds for estate planning and potential inheritances can be part of financial planning.

Retirement Budget Guidance: The Bottom Line

Creating a retirement budget involves a detailed review of income sources, essential expenses, discretionary spending, and long-term planning. Regularly reviewing and adjusting your budget can help you stay on track and adapt to financial changes throughout retirement.

Recent Posts

Tax Diversification in Retirement: Building Flexibility for Future Income Needs

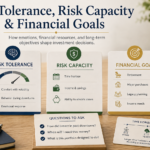

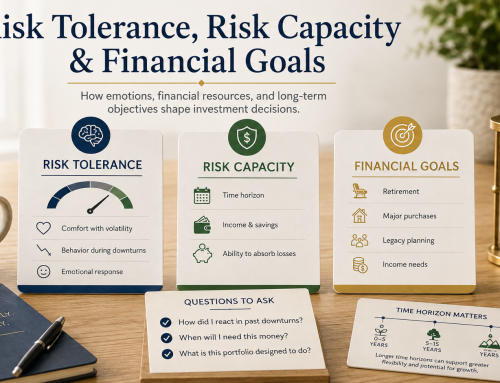

Tax Diversification in Retirement: Building Flexibility for Future Income Needs Understanding the Difference Between Risk Tolerance, Risk Capacity, and Financial Goals

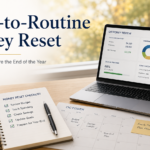

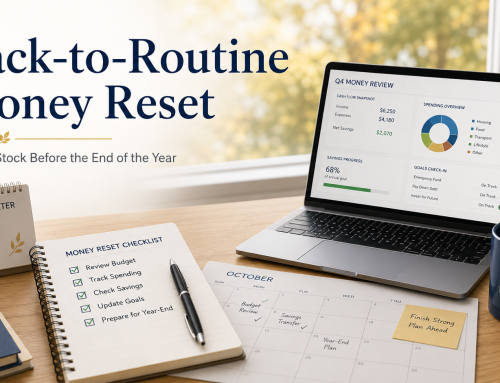

Understanding the Difference Between Risk Tolerance, Risk Capacity, and Financial Goals Back-to-Routine Money Reset: Taking Stock Before the End of the Year

Back-to-Routine Money Reset: Taking Stock Before the End of the Year Scam of the Month: This Job Won’t Work

Scam of the Month: This Job Won’t Work Planning for Longevity: Preparing for a Retirement That May Last Decades

Planning for Longevity: Preparing for a Retirement That May Last Decades Why Putting Your Financial Strategy in Writing Matters

Why Putting Your Financial Strategy in Writing Matters Summer Financial Checkup: Reviewing Your Progress and Priorities

Summer Financial Checkup: Reviewing Your Progress and Priorities- Scam of the Month: FIFA Phishing

Four Financial Scams Targeting Seniors

Four Financial Scams Targeting Seniors- Scam of the Month: Fake It ‘Til They Take It

- How Much Do You Really Need to Retire?

How to Prioritize Multiple Financial Goals at Once

How to Prioritize Multiple Financial Goals at Once The Pros and Cons of Consolidating Investment Accounts

The Pros and Cons of Consolidating Investment Accounts Rethinking Retirement Timing: “Traditional” Retirement?

Rethinking Retirement Timing: “Traditional” Retirement? Mid-Year Tax Planning: Strategies to Consider Before The Fall

Mid-Year Tax Planning: Strategies to Consider Before The Fall

Megan Jones joined the ILG Financial team in 2020 as marketing director. Megan and her husband live in Fredericksburg, VA with their German Short Haired Pointer, Gus. Megan is a graduate of Longwood University and holds a degree in communications. Megan is the oldest of Dave Lopez’s three children and not only enjoys working alongside her father, but also with her cousin, Chase, who joined the ILG Financial team in 2020 as an advisor. Megan is also a fully licensed Life, Health, and Annuity agent. When not at work, Megan enjoys sitting on the back porch with family and friends enjoying food and music.

Megan Jones joined the ILG Financial team in 2020 as marketing director. Megan and her husband live in Fredericksburg, VA with their German Short Haired Pointer, Gus. Megan is a graduate of Longwood University and holds a degree in communications. Megan is the oldest of Dave Lopez’s three children and not only enjoys working alongside her father, but also with her cousin, Chase, who joined the ILG Financial team in 2020 as an advisor. Megan is also a fully licensed Life, Health, and Annuity agent. When not at work, Megan enjoys sitting on the back porch with family and friends enjoying food and music. Amy Anderson joined the ILG Financial team in 2023 as the client relations coordinator. Her responsibilities include scheduling of appointments, annual check-up notifications, and annuity and required minimum distribution assistance. She is a graduate of Harding University with a degree in Computer Information Systems. Amy and her husband have two children and she enjoys reading, crocheting, music and spending time with her family.

Amy Anderson joined the ILG Financial team in 2023 as the client relations coordinator. Her responsibilities include scheduling of appointments, annual check-up notifications, and annuity and required minimum distribution assistance. She is a graduate of Harding University with a degree in Computer Information Systems. Amy and her husband have two children and she enjoys reading, crocheting, music and spending time with her family. Terri Center joined the ILG Financial team in 2019 as client services manager. She handles client records, application processing, and gathering information to provide a professional and friendly experience with all of our clients. Terri is a graduate of Oakland University. She is married and has two children. She enjoys hiking, family time, and puzzle challenging video games. She also likes to share her creativity in her canvas paintings and sewing projects.

Terri Center joined the ILG Financial team in 2019 as client services manager. She handles client records, application processing, and gathering information to provide a professional and friendly experience with all of our clients. Terri is a graduate of Oakland University. She is married and has two children. She enjoys hiking, family time, and puzzle challenging video games. She also likes to share her creativity in her canvas paintings and sewing projects. Jessica Carson joined the ILG Financial team in 2018 as an agent. Jessica and her husband have four children, two dogs, 3 barn cats, 5 chickens, and three parakeets. She indeed loves her children and pets! When not at work, Jessica enjoys playing the piano and cello as well as traveling and spending time outside with her family, hiking, fishing, and boating.

Jessica Carson joined the ILG Financial team in 2018 as an agent. Jessica and her husband have four children, two dogs, 3 barn cats, 5 chickens, and three parakeets. She indeed loves her children and pets! When not at work, Jessica enjoys playing the piano and cello as well as traveling and spending time outside with her family, hiking, fishing, and boating.